Effective Ways to Budget with Our Home Loan Interest Rate Comparison Tools

Home loan interest rates determine how much a borrower ultimately pays for a property loan and influence monthly repayments and the affordability of residential property purchases.

Mortgage interest rates in Singapore are dependent on market benchmarks, loan packages, and financial institution policies. Understanding how to compare these options can help you estimate repayments more accurately and build a realistic housing budget.

This is why mortgage brokers such as mortgageplus offer interest rate package comparison tools so you can evaluate different loan structures, assess repayment scenarios, and identify potential cost changes under different rate conditions. This article will cover how these tools can support informed financial decision-making.

Understanding Mortgage Interest Rates in Singapore

Mortgage interest rates represent the percentage charged by lenders for borrowing funds to finance a property purchase. These rates determine the cost of housing loans issued by banks and financial institutions.

Mortgage interest rates in Singapore typically fall into two broad categories: fixed and floating rates. Each structure influences repayment and financial planning differently.

- A fixed home loan interest rate remains unchanged for a predetermined period, often between two and five years. This structure provides predictable monthly repayments during the fixed period.

- Floating rates, on the other hand, adjust periodically based on benchmark indicators such as interbank lending rates or internal bank reference rates. As benchmarks change, borrowers may experience increases or decreases in monthly repayments.

What Home Loan Interest Rate Comparison Tools Do

Home loan interest rate comparison tools are digital resources that help borrowers evaluate multiple loan options and convert loan variables into projected monthly repayments and long-term cost estimates.

In Singapore, comparison tools simplify complex loan calculations and allow users to examine how different mortgage interest rates affect housing budgets over the life of the loan. These tools typically analyse the following:

- Loan amount

- Interest rate structure

- Loan tenure

- Estimated monthly repayment

- Total interest payable over time

By standardising these inputs, borrowers can compare mortgage packages and identify the financial impact of each option.

Why Interest Rate Comparisons Support Better Budgeting

Budgeting for a property purchase requires accurate repayment projections. Mortgage interest rate comparisons provide a clearer understanding of long-term housing costs before committing to a loan.

In Singapore's property market, even small changes in home loan interest rates can affect repayment levels over a multi-decade loan tenure. A comparison tool helps borrowers visualise these differences and prepare financially.

The budgeting benefits of rate comparison include:

- More accurate monthly repayment estimates

- Improved understanding of total interest costs

- Better planning for income allocation

- Reduced risk of financial over-commitment

Using comparison tools during the early planning stage allows homebuyers to align property affordability with their long-term financial capacity.

Key Factors That Influence Mortgage Interest Rates in Singapore

Both global financial conditions and domestic banking practices influence mortgage interest rates in Singapore. These factors determine how lenders structure home loan packages. Several economic variables contribute to the movement of mortgage interest rates:

- Global interest rate trends

- Interbank lending benchmarks

- Monetary policy conditions

- Banking sector funding costs

- SORA rate fluctuations

Changes in these factors can affect floating loan packages more quickly than fixed-rate loans. Borrowers who understand these influences can better anticipate potential rate fluctuations when budgeting.

How Loan Tenure Affects Monthly Budgeting

Loan tenure refers to the total duration over which a mortgage is repaid. In Singapore, housing loans commonly range from 20 to 30 years, depending on borrower eligibility and financial planning preferences.

The length of the loan tenure directly influences monthly repayment levels and total interest costs. Longer tenures generally result in lower monthly repayments but higher total interest paid over time.

Shorter loan tenures create higher monthly obligations but reduce long-term interest expenses. When evaluating mortgage interest rates, borrowers should consider how tenure interacts with the home loan interest rate to determine overall affordability.

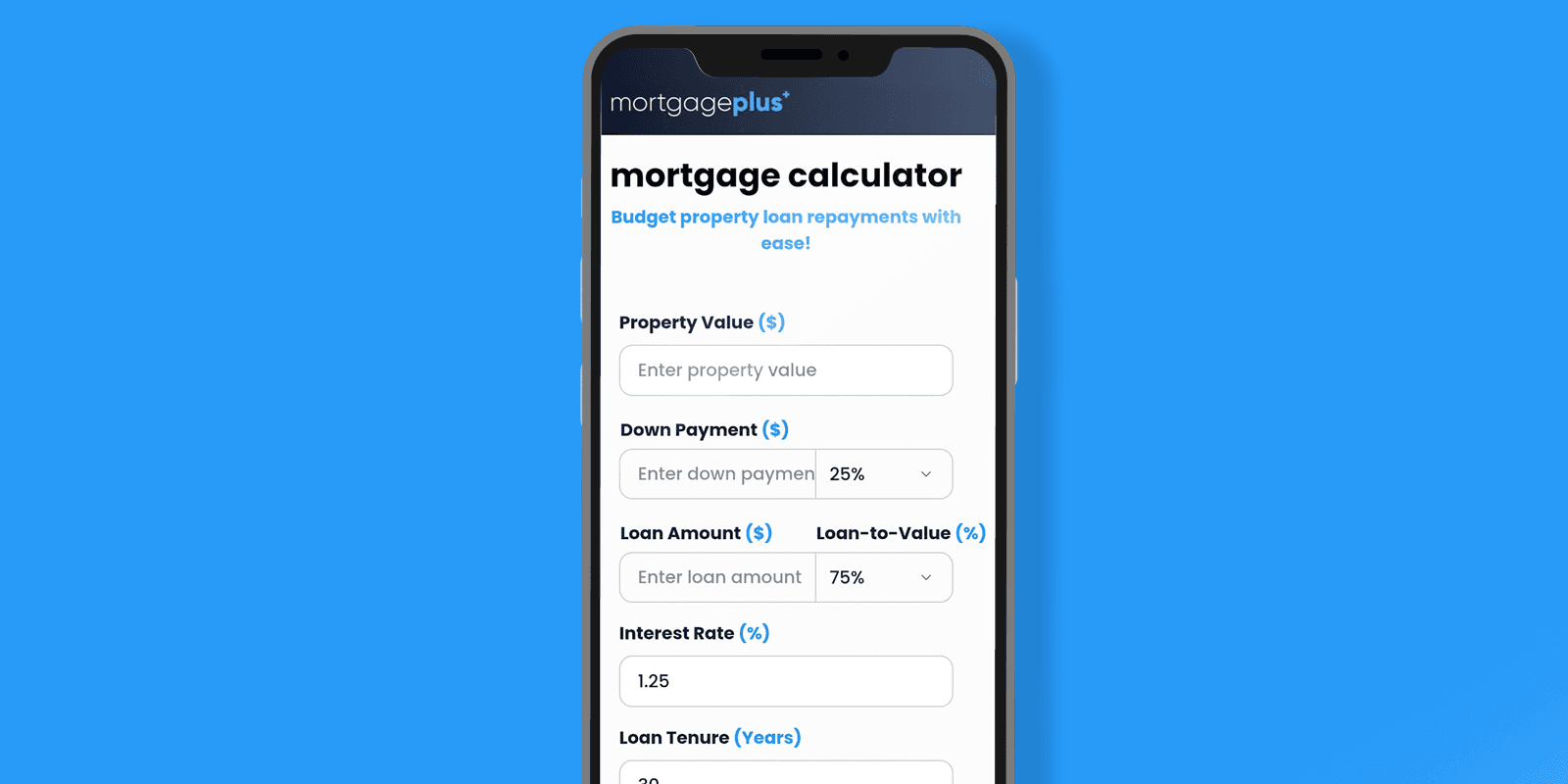

Using Comparison Tools to Estimate Monthly Repayments

Comparison tools estimate monthly repayments by combining loan variables with projected interest rate structures. The mortgageplus calculating tools provide a simplified view of how different loan packages affect budgeting.

A typical repayment estimate requires these inputs that enable our calculators to generate realistic projections based on a borrower's circumstances:

- Property purchase price

- Down payment amount

- Loan amount required

- Interest rate structure

- Loan tenure

Once these values are entered, the tool calculates expected monthly repayments and provides a breakdown of repayment components. These projections can help you evaluate whether a loan fits within your household budget.

Budget Planning for Interest Rate Changes

Interest rate changes can affect long-term mortgage affordability, particularly for floating-rate loans. Budget planning should therefore account for potential rate increases during the loan tenure.

Borrowers often use comparison tools to model different interest rate scenarios. This approach can help you understand how repayment obligations may shift under changing market conditions. Scenario analysis typically includes projections such as:

- Current interest rate repayment estimate

- Moderate interest rate increase scenario

- Higher interest rate stress test

Preparing for multiple scenarios supports a more resilient financial planning and reduces the risk of repayment strain.

Fixed vs Floating Rates in Budget Planning

Floating and fixed mortgage structures offer different advantages for budgeting. Each option provides a different balance between repayment certainty and flexibility. Fixed rates provide repayment stability for the duration of the fixed period. Borrowers know the exact repayment amount during that timeframe.

Floating rates allow repayments to adjust according to market benchmarks. This structure may offer lower initial rates but introduces variability in long-term budgeting.

When using comparison tools, borrowers can analyse how each structure influences repayment patterns and financial flexibility.

How Property Buyers in Singapore Use Comparison Tools

Home buyers in Singapore commonly use mortgage comparison tools during the early stages of property planning. These support data-driven decision-making before approaching lenders. Follow this process when evaluating home loan interest rates:

- Estimate the property purchase price and required loan amount.

- Enter the loan tenure and expected down payment.

- Compare repayment projections across different mortgage interest rates.

- Review how changes in interest rates affect long-term repayments.

This approach allows you to evaluate affordability and narrow down suitable loan packages.

Limitations of Mortgage Comparison Tools

Mortgage comparison tools provide useful projections but do not replace formal loan assessments conducted by lenders. Actual loan terms may vary depending on individual financial profiles.

These tools typically rely on estimated interest rates and standardised loan assumptions. As a result, projections may not include all lending conditions applied by banks. Factors that may influence final loan terms include:

- Borrower income profile

- Credit history

- Loan-to-value ratios

- Property type

Borrowers should therefore treat comparison results as preliminary estimates used for budgeting and planning.

FAQ

- How does a home loan interest rate affect monthly repayments?

A home loan interest rate determines the interest portion of each mortgage repayment. Higher rates increase monthly repayment amounts, while lower rates reduce them. Over a long loan tenure, small rate changes can significantly affect total interest costs. - Why should borrowers compare mortgage interest rates?

Comparing mortgage interest rates helps borrowers understand how different loan packages affect their long-term housing budget. Comparison tools allow borrowers to evaluate repayment projections and identify loan structures that align with their financial capacity. - Do mortgage interest rates change frequently in Singapore?

Mortgage interest rates may change depending on financial market conditions and benchmark movements. Floating-rate loans typically adjust more frequently, while fixed-rate loans remain stable for the duration of the fixed period. - Are comparison tools accurate for budgeting?

Our interest rate comparison tools provide useful repayment estimates based on standard loan assumptions. However, actual loan terms may vary depending on the borrower's eligibility and the lender's policies; therefore, it's best to get the advice of a mortgage broker.

Budget For Your Home Loan with mortgageplus

Mortgage interest rates play a central role in determining the affordability of property financing. Understanding how mortgage interest rates work in Singapore and comparing different packages can help home buyers estimate monthly repayments better.

Home loan interest rate comparison tools provide structured insights into repayment projections, interest costs, and budgeting scenarios. When used the right way, our tools support informed housing decisions and clearer financial planning.

If you want a clearer understanding of how mortgage interest rates affect your property budget, consider consulting our experts at mortgageplus!