Navigate These Hidden Costs to Procure the Best Home Loan in Singapore

Still think comparing headline interest rates is enough to secure the best home loan in Singapore? While interest rates and loan tenure are often the first considerations, there are several additional costs that can significantly affect your overall affordability. These include professional fees, statutory charges, penalties for early repayment, and administrative costs.

Understanding these hidden costs before you commit can help you plan your finances more accurately and avoid unexpected expenses later in your property ownership journey. Learn how getting the assistance of mortgage brokers such as mortgageplus can help untangle these complexities.

Why Hidden Costs Matter When Choosing a Home Loan in Singapore

When deciding on the best home loan, Singapore homebuyers often place their focus on interest rates and repayment terms. However, interest is just one part of the total cost. Hidden costs can add thousands of dollars to the total expenditure over the life of the loan, directly impacting how much you pay. Without clarity on these charges, total borrowing costs can be higher than expected, reducing the financial benefits of a supposedly good deal.

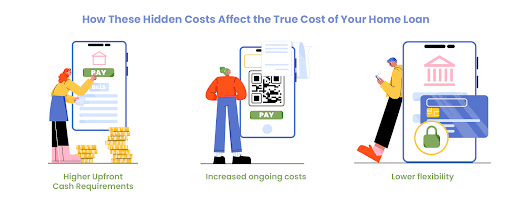

How These Hidden Costs Affect the True Cost of Your Home Loan

Hidden costs influence affordability in these ways:

- Higher upfront cash requirements: Some costs need to be paid at or before loan drawdown, increasing the cash you must have ready.

- Increased ongoing costs: Fees built into the loan structure can raise the effective interest rate you pay over time.

- Lower flexibility: Penalties for early repayment can make switching loans or refinancing costly.

By understanding these costs early, you can compare home loan offers on a more consistent basis and make better financial decisions.

Legal Fees: The Often Overlooked Cost of Home Financing

Legal fees are an unavoidable part of the home loan process in Singapore. These fees cover conveyancing work, mortgage documentation, title searches, and registration with the Singapore Land Authority.

Typical legal fees for a standard residential property mortgage can range from around S$2,000 to S$3,000, depending on the complexity of the property purchase and the law firm engaged. Some banks may offer legal subsidies, but these can come with conditions that could affect you if you refinance early.

Engaging a reputable lawyer early in the process ensures that property and loan documents are properly vetted. Basic details on legal fees can be discussed with home loan advisory companies, such as mortgageplus to aid in a smoother and more cost-effective legal processing.

Valuation Fees and When You’ll Need to Pay Them

Before a bank approves a home loan, the property must typically be professionally valued to confirm its market value and justify the loan amount. This valuation fee is charged by the professional valuer engaged by the bank or independent panel.

Valuation fees generally range from approximately S$200 to S$1,000, depending on the property type and location. If you are refinancing with a new lender, you may need a fresh valuation, which means another valuation cost.

Some banks offer valuation subsidies, but these may not always cover the full fee, and any rebate could be clawed back if you refinance within a defined period. Always check the terms carefully before assuming the valuation will be free.

Stamp Duties and Regulatory Charges You Should Budget For

Stamp duties are statutory charges imposed by the Singapore government on property transactions and loan documents. The main ones to consider include:

- Buyers Stamp Duty (BSD): Charged based on the property purchase price or market value, whichever is higher.

- Additional Buyer’s Stamp Duty (ABSD): Applicable if you are buying additional residential properties or fall into certain buyer categories.

- Stamp duty on the mortgage instrument: This is a separate charge for stamping the loan documents.

Stamp duties must be paid within a set period after the agreement’s execution and can add a significant amount to your initial home purchase costs.

Understanding Early Repayment and Lock-In Penalties

Before agreeing to a home loan package, it’s important to understand penalties and lock-in clauses associated with refinancing or repaying your loan early. Many home loan packages in Singapore include a lock-in period, commonly ranging from two to five years.

If you refinance, switch lenders, or repay your loan within this period, you may incur penalties. Typical early repayment penalties are often calculated as a percentage of the outstanding loan amount, for example, around 1.5% of the remaining loan.

Common scenarios that could trigger penalties

These charges can materially affect your cash flow and savings, especially if you were planning to take advantage of lower interest rates or better terms.

- Selling your property before the lock-in ends

- Refinancing to a different lender within the lock-in period

- Making full or partial repayment early

Refinancing Costs That Can Impact Long-Term Savings

Refinancing means means replacing your existing home loan with a new one to take advantage of lower rates or better terms. While refinancing can reduce monthly repayments and total interest costs, it comes with costs that need to be weighed against the potential savings, such as:

- Legal fees

- Valuation charges

- Administrative fees charged by the new lender

- Penalties for ending your original loan within a lock-in period

Even if you find a lower interest rate, refinancing may not lead to savings if associated costs are high. It’s important to estimate all refinancing costs and compare them against the projected interest savings over time.

Administrative and Processing Fees Lenders Don’t Always Highlight

Some charges are billed as administrative or processing fees by banks, and they cover the cost of assessing and setting up your loan. Typical administrative charges lenders might levy include loan processing fees, documentation handling fees, and facility management charges.

These can range from a few hundred to over a thousand dollars, depending on the lender’s policies. Even if a bank advertises no processing fees, other associated administrative charges may still apply, therefore, always ask for a full list of applicable charges before you commit.

How mortgageplus Helps Navigate Hidden Charges

At mortgageplus, we are a home loan advisory company in Singapore who assist homebuyers and homeowners in comparing home loan packages across banks and financial institutions. We offer:

- Tools to compare interest rates and mortgage calculators

- Access to in-principle approvals that clarify borrowing capacity

- Guidance on lock-in penalties, valuation, and legal fees

- Support through application, documentation, and refinancing decisions

FAQ

- Are mortgage broker services free?

Generally, mortgage brokers like mortgageplus do not charge borrowers directly. They are typically compensated by lenders. - Can foreigners apply for home loans in Singapore?

Foreigners can apply, though eligibility criteria and loan terms may differ from those for Singapore citizens or permanent residents. - What fees should I budget for besides interest?

Include legal fees, valuation fees, stamp duties, administrative charges, and potential penalties for early repayment. - When should I consider refinancing?

Consider refinancing when your lock-in period ends, market rates are lower, or if your financial situation has changed, but always factor in associated costs before deciding.

Get The Best Home Loan in Singapore Without Financial Surprises

Understanding the full cost of a home loan in Singapore goes beyond comparing interest rates. Being aware of legal fees, valuation charges, administrative costs and penalties helps you make more informed decisions.

For a clearer view of your options and to navigate hidden charges with industry insight, contact mortgageplus, our mortgage advisors will help you find a suitable loan package that aligns with your financial goals.