How Often Should You Review Home Loan Interest Rates in Singapore?

Choosing an ideal home loan interest rate and knowing when to review it can make a significant difference to your long-term financial outcomes. Singapore’s mortgage landscape is shaped by changing benchmark rates and economic factors, meaning the rate you secured years ago may not be the best today.

Regularly reviewing loan terms can help you identify opportunities to reduce repayments, from switching between fixed and floating rates to refinancing. This article will explore why reviewing matters, when to act and how rate comparison tools can help.

Why Review Your Home Loan Interest Rate?

Reviewing your Home Loan Interest Rate is not just about chasing a lower figure; it is about ensuring your loan structure continues to meet your financial goals and adapts to market movements. Even small shifts in rates can affect monthly repayments and total interest paid over the loan term. A periodic review ensures that you are not overpaying and you understand whether your current package still fits your circumstances.

Market Trends: How Interest Rates in Singapore Change Over Time

Home loan rates in Singapore have shown notable shifts in recent years. These shifts are usually influenced by global monetary policy and domestic economic conditions. For example, floating rates are typically linked to SORA (the Singapore Overnight Rate Average), which moves with broader financial conditions.

Recent data from the Monetary Authority of Singapore (MAS) shows SORA at around the low-1% range in early 2026, a level markedly lower than the 2.5–3% range seen during earlier peak rate periods. This suggests that current Home Loan Interest Rates in Singapore are generally more affordable compared with recent years. Watching these trends can help you decide whether your existing rate remains competitive or ripe for review.

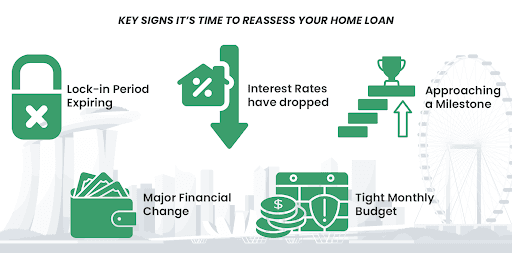

Key Signs It’s Time to Reassess Your Home Loan

- Your lock-in period is nearing expiry

- Market interest rates have dropped significantly

- You are approaching a milestone (e.g., bonus or income change)

- You are financially planning a major change (e.g., renovation or investment)

- Your current repayments strain your monthly budget

These can signal that an adjustment, whether refinancing or switching rate types, could help improve your loan repayments.

Fixed vs Floating Rates: When Should You Review Each?

Fixed and floating Home Loan Interest Rates each have different review triggers.

Fixed rates — provide stability for a set period, shielding you from short-term interest fluctuations. You should review fixed-rate packages as your lock-in period approaches its end to assess whether switching to a new fixed package, repricing with your current lender, or moving to a floating rate makes sense.

Floating rates — move in line with market benchmarks like SORA. These rates can be reviewed more frequently, at least annually, because your repayments will vary directly with market changes. A regular review ensures you stay aware of current SORA levels, spreads offered by lenders and any opportunities to switch if rates rise or fall significantly.

How Often Should Singapore Homeowners Review Their Loan?

For most Singapore homeowners, a structured review every 6 to 12 months is sensible. This frequency ensures you stay informed about competitive interest rate offerings and economic shifts without overreacting to short-term volatility.

To find the best Home Loan Rates Singapore Comparison, use comparison tools to simplify the process. Tools such as mortgage calculators and rate comparison platforms allow you to benchmark your current rate against live offers from banks. These comparisons can highlight cost-saving opportunities and support decisions about refinancing or repricing your home loan.

Common Mistakes to Avoid When Reviewing Home Loan Interest Rates

When reviewing your home loan, avoiding these mistakes can help make measured decisions, rather than reactive ones that might not deliver meaningful benefits. Try to steer clear of these common errors:

- Focusing solely on headline interest rates

- Ignoring lock-in periods or early repayment penalties

- Overlooking other loan features, such as free repricing options

- Neglecting to compare total repayment costs

- Failing to consider your personal financial situation

The Impact of Refinancing on Long-Term Repayments

Refinancing your home loan means replacing your existing loan with a new package, potentially from a different lender. The main reason to refinance is to secure a lower interest rate, which can reduce monthly repayments and, over time, lower the total interest you pay.

Homeowners can also use refinancing to adjust loan tenure, switch rate types, or tap home equity for other financial needs. However, the savings from refinancing should be weighed against associated costs and the time over which you will hold the loan.

Costs to Consider Before Refinancing

Before refinancing, be sure to understand the associated costs, which can include:

- Early termination fees on your existing loan

- Legal and administrative fees for the new loan

- Valuation charges

- Potential changes to your repayment schedule

These costs can offset some of the savings from a lower interest rate, so it’s important to run a thorough calculation before committing to refinance.

How mortgageplus Helps Homeowners Optimise Their Home Loans

At mortgageplus, we offer support for homeowners looking to secure or review their home loans. We provide access to a plethora of bank offers to help you narrow down the best Home Loan Rates Singapore Comparison and comparison tools that let you evaluate Home Loan Interest Rates and packages across banks. Our platform also includes online tools such as mortgage and TDSR calculators, which help you estimate repayments and borrowing capacity.

Our consultants can assist with interpreting comparison results, assessing refinancing options, and guiding you through the application process, including paperwork with lenders. This support can clarify the implications of different rate packages and help you make informed decisions aligned with your financial goals.

FAQ

- How often should I check home loan interest rates?

Aim to review your Home Loan Interest Rate at least every 6 to 12 months, and especially as your lock-in period nears its end. - Does refinancing always save money?

Not always. Potential savings should be balanced against refinancing costs and how long you plan to hold the new loan. - What’s the difference between fixed and floating rates?

Fixed rates stay constant for a set period, while floating rates vary with market benchmarks like SORA. - Can I switch lenders before my lock-in period ends?

You can, but early termination fees or penalties may apply. Always evaluate the cost-benefit before doing so. - Are online mortgage comparison tools accurate?

They provide indicative comparisons and are useful for benchmarking, but always confirm details directly with our mortgageplus advisors.

Plan Regular Loan Reviews with mortgageplus for Long-Term Savings.

For personalised support in reviewing your mortgage, consult our mortgage advisors and make your next review count!