|

Partial Principal Prepayment - An often-overlooked strategy in mortgage savings

|

|

|

|

With much focus on interest rate trends, finding the lowest rates, and even anticipating FED rate cuts, many overlook one of the most effective ways to reduce total interest paid on a home loan - lump sum principal prepayment.

|

|

While analysing and anticipating economic and market factors are important when trying to observe trends in interest rates, it often gives us a short-sighted view and results in short-lived savings when choosing loan packages offered.

|

|

Principal prepayment within the loan tenure chosen involves making lump-sum repayments toward the outstanding loan balance and can have a far greater impact on interest savings. These lump-sum repayments can come from bonuses or extra savings, after setting aside buffer funds based on one's financial goals.

|

|

|

|

Home loan instalments consist of two components: principal (P) and interest (I). Interest is calculated on a lower principal outstanding each month when monthly instalments are paid. By making periodic lump sum partial prepayments, the principal outstanding will be lowered, and hence, interest is calculated based on the lower loan amount outstanding.

|

|

|

|

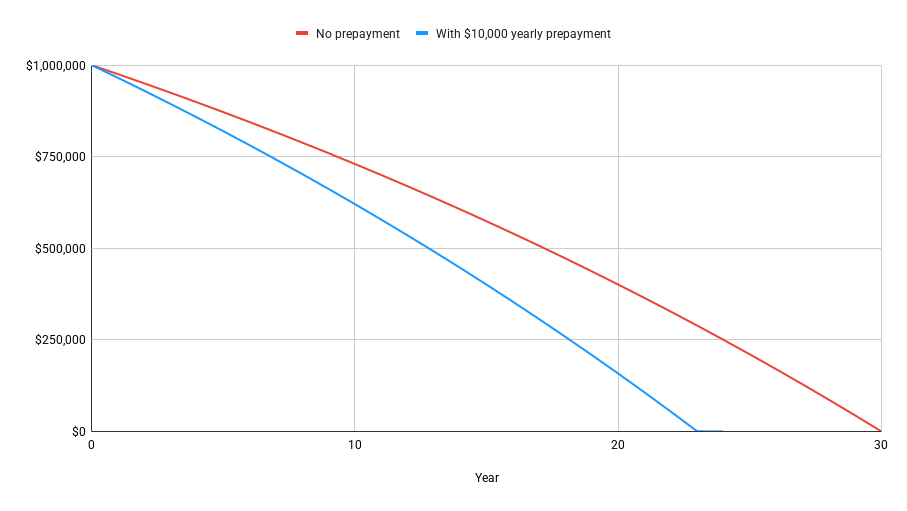

• $1,000,000 home loan with 30 years loan tenure

|

|

|

|

• Making $10,000 lump sum payments yearly*

|

|

|

|

• Assume 2% p.a. interest rates

|

|

|

|

*Assumption: Calculation based on monthly rest and prepayments made yearly at the beginning of the year

|

|

|

| Scenario | Total Interest Paid | Effective Loan Duration |

|---|

| No yearly prepayment | $330,630 | 360 months

(30 years) | | $10,000 yearly prepayment | $244,750 | 275 months

(22 years, 11 months) |

|

|

|

|

• Total interest saved: ~$85,880

|

|

|

|

• Loan shortens by: ~85 months (7 years and 1 month)

|

|

|

|

Essentially, by paying $10,000 yearly towards your home loan, you reduce the overall interest paid by $85,880 and finish your loan 7 years earlier.

|

|

|

|

Direct benefits include higher interest savings, especially when partial prepayments are used to complement other interest-savings strategies such as refinancing or repricing. When combined, these approaches can result in even greater overall savings.

|

|

|

|

Indirect benefits include the ability to become debt-free sooner and own a fully paid asset for legacy planning. Homeowners also retain the option to take up a reverse mortgage in the future to unlock equity, if needed.

|

|

|

|

In addition, the reduced debt obligations translate into cash on hand for other investment opportunities or a stronger focus on retirement planning.

|

|

|

|

In times when borrowing becomes more expensive due to increasing interest rates and investment returns are lower, it may make more financial sense to pay down your mortgage faster. By making extra payments toward the principal, you essentially reduce the total interest paid during the duration of the loan tenure.

|

|

|

|

On the other side of the same coin, when interest rates are low and investment returns are higher, we can look for other investment opportunities with a higher rate of return.

|

|

|

|

Your financial goals, investment objectives and risk appetite can help you decide the amount of partial principal prepayment that you can make and its frequency, without compromising your liquidity.

|

|

|

|

If this interest savings strategy fits one's financial goals, do look out for loan packages that allow partial principal repayments without penalty.

|

|

|

|

As a mortgage broker, we support clients across their home-financing journey and regularly share insights on the best home loan packages across banks, mortgage trends, lending policies and the property market.

|

|

|

|

If you are curious how this strategy could work for you, our mortgageplus experts are happy to find a tailored solution.

|

|

|

|